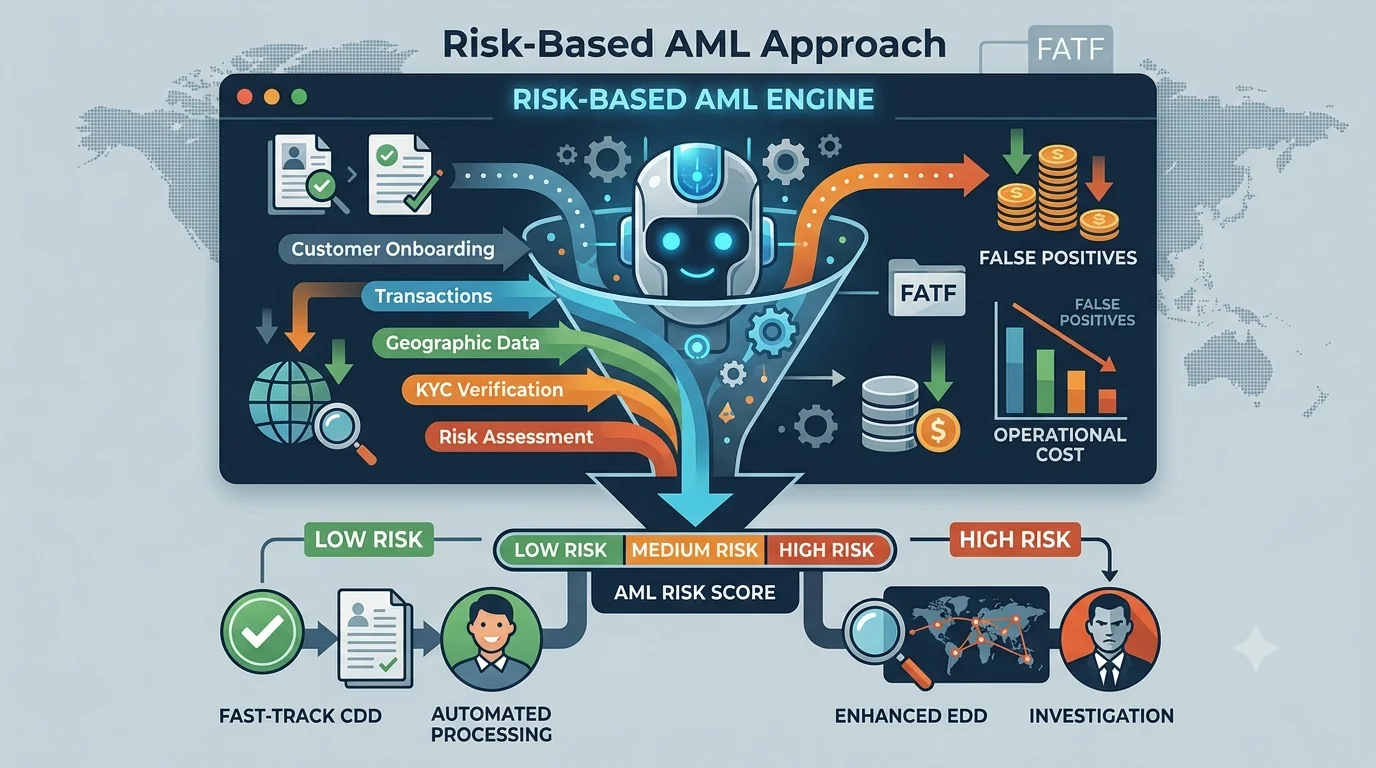

A risk-based AML approach is a compliance methodology that allocates Anti-Money Laundering (AML) controls according to the level of risk posed by customers, businesses, transactions, and jurisdictions. Rather than treating every customer the same, organizations apply enhanced scrutiny to higher-risk relationships while simplifying checks for lower-risk customers.

This approach helps financial institutions improve compliance efficiency, reduce false positives, and focus resources where they are needed most.

The risk-based approach is recommended by the Financial Action Task Force (FATF) and has become a cornerstone of modern AML and KYC compliance programs worldwide.

What Is a Risk-Based AML Approach?

A risk-based AML approach allocates compliance resources according to the level of money laundering risk presented by customers, businesses, transactions, and jurisdictions. Instead of applying identical procedures to every relationship, organizations tailor Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD) based on assessed risk levels.

This methodology is central to effective AML compliance software for financial institutions, enabling teams to prioritize investigations, streamline onboarding, and maintain regulatory alignment at scale.

Why Traditional AML Programs Struggle

Many organizations still apply identical compliance procedures to every customer.

While this may appear thorough, it often creates significant challenges:

- Excessive manual reviews

- High operational costs

- Slow onboarding processes

- Large numbers of false positive alerts

- Inefficient allocation of compliance resources

When compliance teams spend valuable time reviewing low-risk customers, they have less capacity to investigate genuinely suspicious activity.

A risk-based AML program solves this problem by prioritizing customers according to their actual risk profile.

How Risk-Based AML Works

A risk-based AML framework evaluates several risk factors before assigning a customer risk rating.

Common factors include:

Customer Risk

Organizations assess whether a customer may present an elevated risk of financial crime.

Examples of higher-risk customers include:

- Politically Exposed Persons (PEPs)

- High-net-worth individuals

- Cash-intensive businesses

- Complex corporate structures

- Customers with adverse media exposure

Geographic Risk

Some countries and jurisdictions carry higher AML risks due to sanctions, corruption concerns, or weak regulatory oversight.

Compliance teams often evaluate:

- Sanctioned jurisdictions

- High-risk FATF countries

- Countries with elevated corruption indexes

- Regions associated with financial crime activity

Product and Service Risk

Certain products naturally present greater money laundering risks.

Examples include:

- Cross-border payments

- Cryptocurrency services

- Correspondent banking

- Trade finance

- High-value transactions

Transaction Risk

Organizations monitor transaction behavior for unusual patterns.

Potential indicators include:

- Unusually large transactions

- Rapid movement of funds

- Unexpected transaction volumes

- Transactions involving high-risk countries

- Structuring activities designed to avoid reporting thresholds

The Risk-Based AML Assessment Process

Most modern AML programs follow a structured workflow:

- Collect customer information during onboarding.

- Verify customer identity through KYC checks.

- Conduct sanctions screening.

- Perform PEP screening.

- Review adverse media results.

- Assess beneficial ownership structures through UBO identification.

- Calculate customer risk scores.

- Apply appropriate due diligence measures.

- Monitor customers continuously.

This process enables organizations to make informed decisions based on actual risk rather than assumptions.

Customer Due Diligence vs Enhanced Due Diligence

A risk-based AML framework relies heavily on Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD).

| Customer Due Diligence (CDD) | Enhanced Due Diligence (EDD) |

|---|---|

| Applied to standard-risk customers | Applied to high-risk customers |

| Basic identity verification | Additional verification and investigation |

| Standard monitoring | Increased monitoring frequency |

| Lower compliance effort | Higher compliance scrutiny |

| Faster onboarding | More detailed risk assessment |

Organizations use AML risk scoring to determine when enhanced due diligence is required.

How Risk-Based AML Reduces False Positives

False positives are one of the most expensive challenges facing compliance teams.

When screening systems generate large volumes of alerts that ultimately prove harmless, investigators spend valuable time reviewing non-risky customers.

A risk-based approach improves alert quality by:

- Prioritizing higher-risk matches

- Applying context to screening results

- Incorporating customer risk profiles

- Improving escalation workflows

- Reducing unnecessary investigations

Modern AML screening platforms combine risk scoring with contextual matching to further reduce noise and improve investigator productivity.

The result is a more efficient compliance operation with better resource allocation.

Benefits of a Risk-Based AML Program

Organizations that implement a risk-based approach typically experience several benefits.

Improved Compliance Efficiency

Compliance teams focus on customers and transactions that require attention rather than reviewing every case equally.

Lower Operational Costs

Reducing manual investigations helps organizations control compliance expenses as they grow.

Faster Customer Onboarding

Low-risk customers can move through business onboarding and retail KYC flows more quickly, improving user experience and conversion rates.

Better Regulatory Alignment

Most regulators expect organizations to demonstrate a documented risk-based compliance framework aligned with FATF risk-based approach guidance.

Stronger Risk Management

Risk-based monitoring improves the ability to identify suspicious activity and emerging threats.

Risk-Based AML vs Rules-Based AML

| Risk-Based AML | Rules-Based AML |

|---|---|

| Focuses on customer risk | Focuses on fixed rules |

| Dynamic risk scoring | Static thresholds |

| Prioritizes high-risk cases | Treats all customers similarly |

| More efficient investigations | Higher false positive rates |

| Scales more effectively | Often requires greater manual effort |

While rules-based controls remain important, modern AML programs increasingly combine them with risk scoring and automated monitoring.

Technology’s Role in Risk-Based AML

Modern AML platforms use automation, machine learning, and real-time data sources to improve risk assessments.

These systems can:

- Screen customers against sanctions lists

- Identify Politically Exposed Persons (PEPs)

- Monitor adverse media

- Verify beneficial ownership structures

- Calculate dynamic risk scores

- Trigger enhanced due diligence workflows

- Support ongoing monitoring

Integrated AML compliance software for financial institutions unifies these capabilities—connecting KYC verification, UBO identification, and AML screening into a single risk-based workflow.

Automation helps organizations maintain compliance while reducing operational burdens.

Industries That Benefit from Risk-Based AML

Risk-based AML frameworks are widely used across regulated industries, including:

- Banks

- Fintech companies

- Payment Service Providers (PSPs)

- Cryptocurrency exchanges

- Insurance providers

- Lending platforms

- Wealth management firms

For corporate and institutional clients, business onboarding (KYB) programs apply the same risk-based principles to verify entities, directors, and beneficial owners before granting access to financial services.

As regulatory expectations continue to increase, risk-based compliance has become a competitive advantage as well as a regulatory necessity.

Frequently Asked Questions

What is a risk-based AML approach?

A risk-based AML approach allocates compliance resources according to the level of money laundering risk presented by customers, businesses, transactions, and jurisdictions.

Why is a risk-based approach important for AML compliance?

It improves compliance efficiency, reduces false positives, lowers operational costs, and helps organizations focus on higher-risk activities.

What factors are considered in AML risk assessments?

Common factors include customer risk, geographic risk, transaction risk, product risk, sanctions exposure, beneficial ownership, and adverse media findings.

What is the difference between CDD and EDD?

Customer Due Diligence (CDD) applies to standard-risk customers, while Enhanced Due Diligence (EDD) involves additional scrutiny for higher-risk individuals and entities.

Does FATF recommend a risk-based approach?

Yes. The Financial Action Task Force (FATF) promotes a risk-based approach as a core principle of effective AML compliance programs.

Can automation improve AML risk assessments?

Yes. Modern AML solutions automate screening, monitoring, risk scoring, and ongoing customer reviews to improve accuracy and efficiency.

Conclusion

A risk-based AML approach allows organizations to focus compliance efforts where they matter most. By combining customer due diligence, risk scoring, sanctions screening, beneficial ownership analysis, and ongoing monitoring, businesses can improve compliance outcomes while reducing operational costs.

As financial crime risks continue to evolve, organizations that adopt risk-based AML frameworks are better positioned to manage risk, satisfy regulators, and create more efficient customer onboarding experiences.