AML screening is the process of checking customers, businesses, and beneficial owners against financial crime risk data sources such as sanctions lists, politically exposed persons (PEP) databases, watchlists, and adverse media reports to identify potential money laundering or terrorist financing risks.

It is a core part of broader compliance frameworks including Know Your Customer (KYC), Customer Due Diligence (CDD), and Enhanced Due Diligence (EDD).

AML screening is commonly used by banks, fintechs, crypto platforms, and payment providers to prevent exposure to financial crime.

Why AML Screening Matters

Financial institutions are required to comply with global standards set by regulators such as the Financial Action Task Force (FATF) and national authorities like Office of Foreign Assets Control (OFAC).

Key risks AML screening helps prevent:

- Money laundering activities

- Terrorist financing

- Fraud and corruption exposure

- Sanctions violations

- Regulatory penalties

Key benefits:

- Regulatory compliance with AML laws

- Reduced financial crime exposure

- Faster and safer onboarding

- Improved customer risk scoring

- Stronger governance under KYC/CDD frameworks

The scale of financial crime

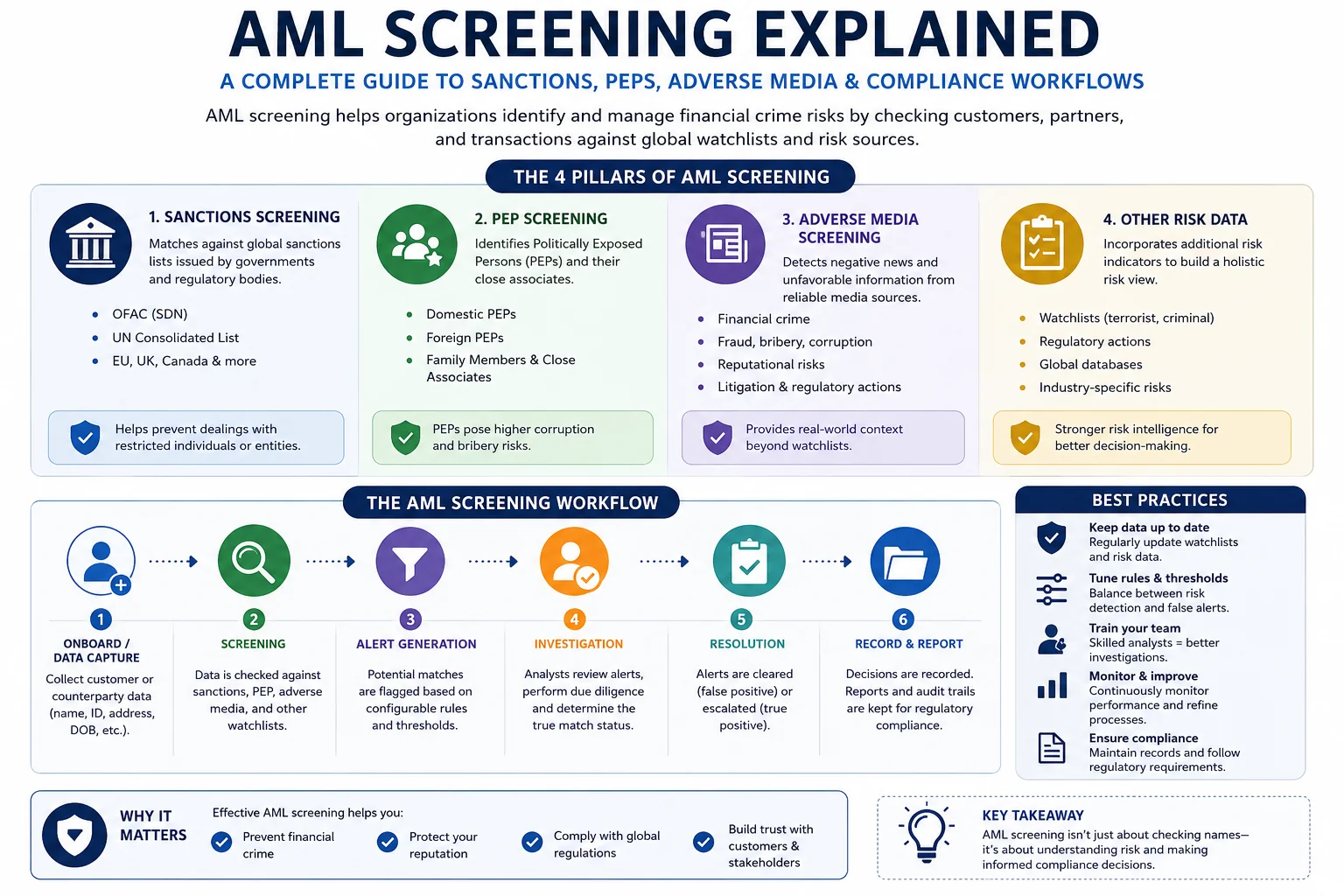

What Are the Three Types of AML Screening?

1. Sanctions Screening

Sanctions screening checks individuals and organizations against global restricted party lists.

It identifies whether a customer is prohibited from doing business under international law.

Common sanctions authorities include:

- United Nations (UN)

- European Union (EU)

- Office of Foreign Assets Control (OFAC)

- UK HM Treasury

Sanctions screening is mandatory during onboarding and ongoing monitoring under AML regulations.

2. PEP Screening

Politically Exposed Person (PEP) Screening identifies individuals holding or linked to prominent public positions.

Examples include:

- Government ministers

- Senior judges

- Military officials

- Heads of state

- State-owned enterprise executives

PEPs are not inherently suspicious, but they carry higher corruption risk and typically require Enhanced Due Diligence (EDD).

3. Adverse Media Screening

Adverse Media Screening scans news, reports, and public data for negative information linked to financial crime risk.

It detects risks such as:

- Fraud allegations

- Money laundering investigations

- Corruption cases

- Terrorism financing links

- Tax evasion reports

- Organized crime associations

Unlike sanctions lists, adverse media often identifies early-stage risk signals before regulatory action is taken.

AML Screening Workflow (Step-by-Step Framework)

Modern compliance teams typically follow this structured workflow:

- Customer identity collection (KYC)

- Identity verification & UBO Identification

- Sanctions screening

- PEP screening

- Adverse media screening

- Risk scoring and classification

- Escalation for compliance review

- Ongoing monitoring & re-screening

This structured approach ensures continuous compliance with global AML regulations.

AML Screening vs KYC (Comparison Table)

| Feature | AML Screening | KYC |

|---|---|---|

| Purpose | Detect financial crime risk | Verify customer identity |

| Focus | Risk monitoring | Identity validation |

| Data sources | Sanctions, PEP, adverse media | Identity documents, biometrics |

| Timing | Ongoing process | Onboarding stage |

| Regulatory scope | AML compliance | Customer verification laws |

AML screening is risk-focused, while KYC is identity-focused.

AML Screening vs Transaction Monitoring

| Feature | AML Screening | Transaction Monitoring |

|---|---|---|

| Focus | Customer risk profiles | Financial activity behavior |

| Timing | Onboarding + ongoing | Post-transaction analysis |

| Detects | Sanctions/PEP/adverse media matches | Suspicious transaction patterns |

| Example | Name appears on OFAC list | Unusual large transfers |

Why Manual AML Screening Fails

1. High False Positives

Common names and weak matching logic generate unnecessary alerts, increasing compliance workload.

2. Slow Onboarding

Manual reviews delay customer activation and reduce conversion rates.

3. Inconsistent Decisions

Different analysts may apply different risk thresholds.

4. Regulatory Exposure

Outdated sanctions lists or missed updates increase compliance risk.

How Automated AML Screening Works

Automated AML systems unify screening across multiple datasets in real time:

- Sanctions list matching

- PEP database checks

- Adverse media analysis

- Risk scoring models

- Automated alert routing

- Continuous monitoring

AI and machine learning improve accuracy by reducing false positives and identifying complex risk patterns. Organizations can deploy these capabilities through integrated AML Screening to automate checks at onboarding and throughout the customer lifecycle.

AML Screening Workflow (Simplified Model)

The AML Screening Workflow:

- Identity collection

- Sanctions screening

- PEP screening

- Adverse media screening

- Risk scoring

- Compliance review

- Ongoing monitoring

This framework is widely used across Know Your Business (KYB) and KYC compliance programs.

Industries That Require AML Screening

AML screening is required in:

- Banking and financial services

- Fintech and digital wallets

- Cryptocurrency exchanges

- Insurance providers

- Payment service providers

- Lending platforms

- Real estate transactions

- Corporate onboarding (KYB processes)

Financial institutions building end-to-end compliance programs often start with dedicated AML Compliance Software for Financial Institutions that unifies screening, case management, and ongoing monitoring.

Best Practices for AML Screening

- Use multiple data sources (sanctions, PEP, adverse media)

- Implement risk-based scoring models

- Automate screening and alerts

- Maintain continuous monitoring

- Integrate AML into KYC/CDD workflows

- Regularly update watchlists and compliance rules

Future of AML Screening

AML compliance is evolving from rule-based screening to intelligent risk detection systems.

Emerging technologies include:

- Artificial intelligence (AI) for match accuracy

- Machine learning for risk scoring

- Graph analytics for hidden relationships

- Behavioral pattern detection

These advancements help compliance teams move from reactive screening to proactive financial crime prevention.

Frequently Asked Questions (FAQ)

1. What is AML screening?

AML screening is the process of checking customers against sanctions, PEP lists, and adverse media to detect financial crime risks.

2. Is AML screening mandatory?

Yes, regulated industries must perform AML screening under global compliance frameworks such as FATF standards.

3. What lists are used in AML screening?

Sanctions lists (OFAC, UN, EU), PEP databases, and adverse media sources are commonly used.

4. What is the difference between AML screening and KYC?

KYC verifies identity, while AML screening assesses financial crime risk.

5. What is ongoing AML screening?

It is continuous monitoring of customers after onboarding to detect new risks.

6. What is a PEP in AML screening?

A PEP is a politically exposed person who may present higher corruption risk due to their public position.

7. What is adverse media screening?

It is the process of identifying negative news or reports related to financial crime risks.

8. How does AML screening reduce fraud?

It identifies high-risk individuals early and prevents onboarding of potentially fraudulent customers.

9. What is the role of sanctions screening?

It ensures businesses do not engage with individuals or entities on restricted lists.

10. Who needs AML screening?

Banks, fintechs, crypto platforms, insurers, and any regulated financial service providers.

Conclusion

AML screening is a foundational pillar of modern compliance frameworks, integrating KYC, CDD, EDD, sanctions screening, PEP detection, and adverse media analysis into a unified risk management system.

Organizations that adopt automated AML screening gain:

- Stronger regulatory compliance

- Reduced financial crime exposure

- Faster onboarding processes

- Continuous customer risk visibility

As financial crime evolves, AML screening is no longer optional—it is essential for protecting both businesses and the global financial system.