The new global way for identity trust

Investor Onboarding in Fund Administration: KYC and AML Requirements in the EU, France, the UK, and Worldwide

In this article:

Summary

- What Is Investor Onboarding?

- Why KYC and AML Matter for Fund Administrators

- Key Steps in the Investor Onboarding Process

- EU, France, and UK Regulatory Framework for Fund Onboarding

- Practical Challenges in Due Diligence for Fund Administrators

- Best Practices and Future Outlook for Investor Onboarding

- Frequently Asked Questions About Investor Onboarding and KYC/AML

- Conclusion: Investor Onboarding as a Pillar of Financial Integrity

Investor onboarding is the gateway through which capital enters the investment fund industry. It may sound procedural, but in practice it is one of the most critical stages of fund administration. Whether you are a fund administrator in Luxembourg, an asset manager in Paris or London, or a compliance officer dealing with cross-border investors worldwide, onboarding is the first line of defence against financial crime.

At the heart of onboarding sit two cornerstones: Know Your Customer (KYC) and Anti-Money Laundering (AML). These checks ensure that funds accept legitimate investors, verify beneficial ownership, and comply with regulatory standards in multiple jurisdictions. In this article, we break down the process, regulations, challenges, and best practices that shape investor onboarding in today’s global financial markets.

What Is Investor Onboarding?

Investor onboarding refers to the process by which a fund administrator or management company (ManCo) reviews and approves new investors before they can invest. It goes far beyond signing a subscription agreement. At its core, onboarding means:

- Verifying the identity of investors, whether individuals or legal entities.

- Understanding the structure and ultimate beneficial ownership (UBO) behind complex entities.

- Assessing the level of risk that each investor poses.

- Screening against sanctions, politically exposed persons (PEPs), and adverse media.

- Ensuring funds are legitimate and derived from lawful sources.

- Setting up ongoing monitoring systems for transactions and re-screening.

This process is legally mandated in the EU, France, and the UK, and broadly recognised worldwide as a cornerstone of AML compliance.

Why KYC and AML Matter for Fund Administrators

KYC and AML requirements are not box-ticking exercises. They are essential to:

- Protecting the financial system from money laundering, terrorist financing, and tax evasion.

- Safeguarding the reputation of investment funds, fund administrators, and fund managers.

- Ensuring compliance with regulatory frameworks such as the EU AML Directives, the Luxembourg AML Law of 2004, and the UK Money Laundering Regulations 2017.

- Maintaining trust with institutional and retail clients while meeting investor expectations through diligent compliance checks and ongoing monitoring.

Regulators across Europe are increasingly adopting a risk-based approach. This means the extent of due diligence must match the investor’s risk profile: a straightforward retail investor requires standard checks, while a politically exposed investor from a high-risk jurisdiction demands enhanced due diligence (EDD).

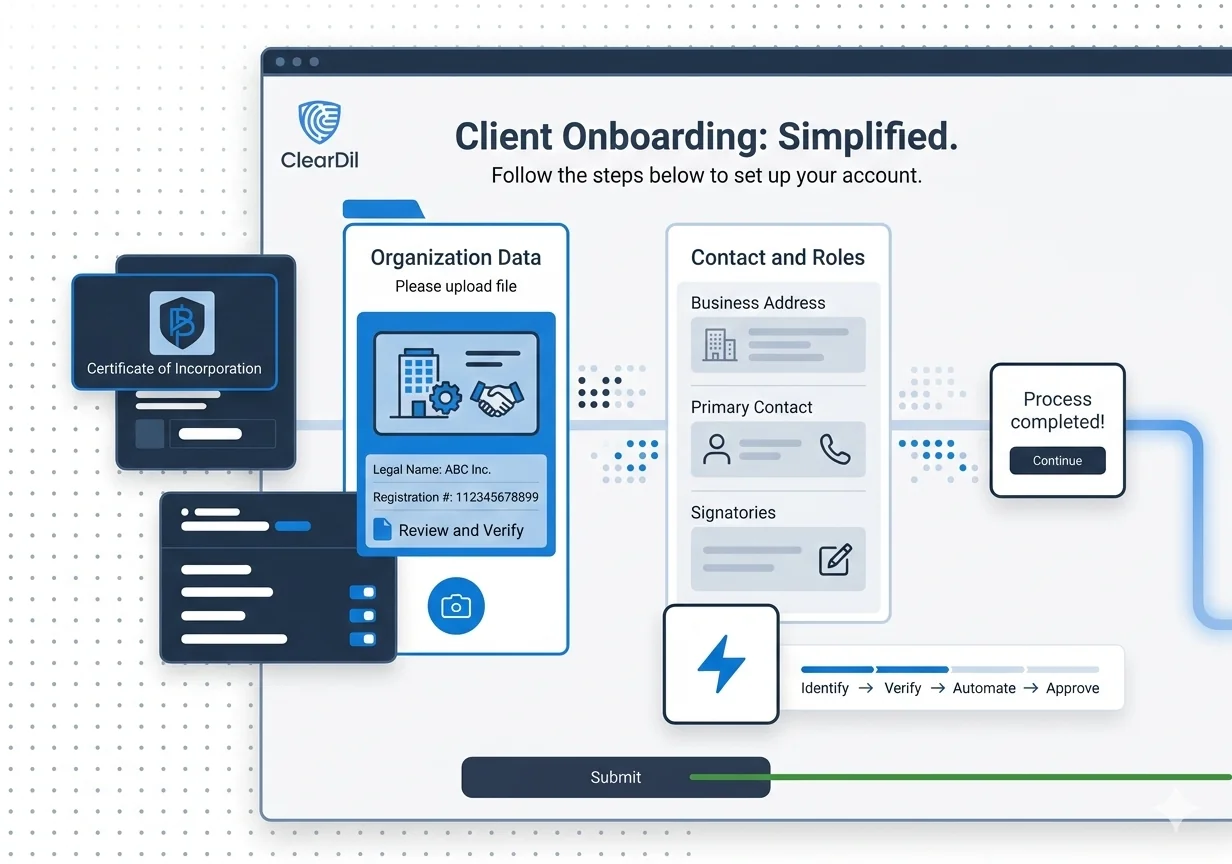

Key Steps in the Investor Onboarding Process

The investor onboarding process is multi-layered, involving both documentation and compliance judgement. Below is a structured overview of the typical workflow in fund administration:

| Step | What Is Done | Why It Matters | Documentation / Outputs |

|---|---|---|---|

| Initial risk screening | Pre-checks for red flags (high-risk country, PEP, sanctions) | Determines level of due diligence required | Risk classification, automated screening reports |

| Identity verification | Individuals: ID, proof of address. Entities: incorporation docs, directors, UBO lists | Satisfies Customer Due Diligence (CDD) obligations | Certified copies, structure charts, UBO declarations |

| Source of funds / wealth | Verify where money and wealth originate | Prevents illicit funds from entering the financial system | Bank statements, financial records, declarations |

| Sanctions / PEP screening | Screening against global watchlists and adverse media | Avoids dealings with restricted or high-risk persons | Screening reports, escalation records |

| Enhanced due diligence (EDD) | Deeper checks for complex entities, PEPs, or high-risk jurisdictions | Regulatory requirement for high-risk cases | Additional verification, senior compliance approval |

| Risk scoring | Assign a risk level based on geography, investor type, and fund source | Determines monitoring frequency | Risk assessment tool, documented rationale |

| Legal / subscription documentation | Ensure all agreements are signed and valid | Ensures eligibility and legal compliance | Subscription agreements, investor questionnaires |

| Final approval | Only after full KYC/AML clearance | Prevents acceptance of non-compliant investors | Compliance sign-off |

| Ongoing monitoring | Regular updates, transaction monitoring, re-screening | Keeps records current, adapts to risk changes | Monitoring reports, refreshed KYC files |

EU, France, and UK Regulatory Framework for Fund Onboarding

European Union: AML Directives and the Rise of AMLA

The EU has developed a robust and evolving AML framework through successive AML Directives, now entering a transformative phase with the establishment of the Anti-Money Laundering Authority (AMLA). AMLA will promote a more data-driven and risk-focused approach to AML supervision, relying on structured data, analytics, and technology-enabled monitoring.

This shift marks a move away from fragmented national supervision towards a centralised and standardised EU AML regime, with direct implications for cross-border investor onboarding. It reinforces:

- A risk-based approach to customer due diligence.

- Clear identification and verification of beneficial ownership.

- Enhanced due diligence for high-risk investors and jurisdictions.

- Ongoing, technology-enabled monitoring, risk assessments, and reporting to prevent financial crime.

Luxembourg: CSSF Supervision and the AML Law of 2004

As one of the world’s largest fund domiciles, Luxembourg enforces the AML Law of 12 November 2004 (as amended). It is supervised by the Commission de Surveillance du Secteur Financier (CSSF), which has issued detailed guidance such as CSSF Regulation 12-02. Even unregulated AIFs must comply because their service providers — custodians, administrators, and banks — are bound by law.

France: AMF KYC and AML Obligations

In France, the Autorité des marchés financiers (AMF) sets out clear obligations for KYC and AML compliance. French law requires strict due diligence around beneficial owners, high-risk jurisdictions, and politically exposed persons (PEPs), in line with EU directives and FATF recommendations.

United Kingdom: FCA and the Money Laundering Regulations 2017

Post-Brexit, the UK continues to align broadly with EU standards under its own legislation. The UK Money Laundering Regulations 2017 (as amended) set the regulatory framework, with supervision carried out by the Financial Conduct Authority (FCA). Firms must apply a risk-based approach to customer due diligence and maintain robust AML compliance programmes.

Practical Challenges in Due Diligence for Fund Administrators

While the rules are clear, real-world practice introduces significant complexity. Fund administrators must navigate multiple challenges:

Timing Delays and Investor Friction

Collecting certified documents from overseas investors can be time-consuming, impacting onboarding speed and investor satisfaction — especially in cross-border fund structures.

Data Quality and Documentation Issues

Expired, incomplete, or improperly certified documents frequently obstruct the KYC process, requiring additional diligence and follow-up with investors or intermediaries.

Complex Ownership Structures

Multi-layered SPVs, trusts, and cross-border holdings complicate the verification of ultimate beneficial owners (UBOs), increasing compliance risk and the risk of inadvertently onboarding high-risk investors.

False Positives in Sanctions Screening

Automated sanctions and adverse media screening tools often generate false hits, necessitating manual review to avoid unnecessary delays and friction in the investor experience.

Evolving AML Regulations

The continuous evolution of EU AML Directives and national AML legislation demands regular updates to onboarding policies and procedures, adding to operational and resource challenges.

GDPR and Data Protection Compliance

Handling sensitive personal and financial information during customer due diligence requires strict adherence to GDPR and local privacy laws to protect investors and maintain transparency.

Best Practices and Future Outlook for Investor Onboarding

Leveraging Technology for Scalable Compliance

To overcome these challenges, fund administrators are increasingly turning to technology-driven onboarding platforms. Automated solutions can:

- Centralise document collection and management to create a single source of truth for all investor information.

- Perform real-time sanctions and PEP screening to detect high-risk investors promptly.

- Provide audit-ready compliance records that meet regulatory requirements and support suspicious activity reports (SARs).

- Reduce manual errors and accelerate approval times through automation and structured enhanced due diligence measures.

Balancing Automation with Human Judgement

Technology is not a replacement for compliance expertise. Complex cases, high-risk investors, and ambiguous ownership structures still require careful review by qualified compliance professionals with sound judgement and regulatory knowledge.

The Global Trend: Harmonisation and Digitalisation

Looking ahead, the global trend is towards regulatory harmonisation and digitalisation. The European Commission is moving towards a centralised AML authority through AMLA, while the UK is emphasising technology-enabled supervision. Globally, regulators are converging on common standards, making cross-border investor onboarding more consistent and more demanding at the same time.

Frequently Asked Questions About Investor Onboarding and KYC/AML

What is KYC in fund administration? KYC (Know Your Customer) in fund administration is the process of verifying the identity of investors, understanding their financial background, and assessing the risks they may pose. It includes identity checks, UBO verification, source of funds analysis, and PEP/sanctions screening.

What is the difference between CDD and EDD? Customer Due Diligence (CDD) is the standard level of verification applied to most investors. Enhanced Due Diligence (EDD) is a deeper investigation required for high-risk investors, such as PEPs, investors from high-risk jurisdictions, or complex multi-layered structures.

Who regulates AML compliance for fund administrators in Europe? In the EU, national competent authorities such as the CSSF in Luxembourg and the AMF in France supervise AML compliance. The newly established AMLA (Anti-Money Laundering Authority) will progressively centralise supervision across the EU. In the UK, the FCA supervises fund managers and administrators under the Money Laundering Regulations 2017.

What is a UBO in fund administration? A UBO (Ultimate Beneficial Owner) is the natural person who ultimately owns or controls an investor entity, typically defined as holding a direct or indirect ownership interest of 25% or more. Identifying and verifying UBOs is a core requirement of KYC for legal entities.

Conclusion: Investor Onboarding as a Pillar of Financial Integrity

Investor onboarding in fund administration is far more than a gatekeeping function. It forms the foundation of financial integrity and regulatory compliance. Through comprehensive KYC and AML checks, fund administrators and fund managers protect their funds, their investors, and the broader financial system from financial crime — including money laundering and terrorist financing.

Across jurisdictions — from Luxembourg’s CSSF regulations and France’s AMF guidelines, to the UK’s FCA requirements and international FATF standards — the principle remains consistent: robust, risk-based customer due diligence and enhanced due diligence measures are essential to mitigate risk and ensure full compliance with AML regulations.

For fund administrators managing complex cross-border business relationships, the challenge lies not only in meeting these regulatory requirements but in doing so efficiently, transparently, and at scale. Modern onboarding platforms, such as those offered by ClearDil, leverage automation and ongoing monitoring to transform investor onboarding into a streamlined, transparent, and investor-friendly process — protecting assets, maintaining reputation, and meeting investor expectations while managing sensitive information securely.